Accounting statements are necessary tools that give an in-depth overview of the financial performance and stability of a company. As an investor, a business owner, a creditor or just a person who wants to know the financial position of a company, being able to read and understand financial statements enables you to make informed decisions using facts and figures, and not by guesswork.

This guide combines the practical wisdom and technical organization of two exhaustive articles to provide you with a balanced picture of financial statements-what they are, how they operate and why they are important.

What are Financial Statements and Why are they Important?

Financial statements are official documents that contain a summary of the financial activities and position of a business in a given time frame. The documents provide a uniform manner in which the stakeholders would be scrutinizing the operations of the company and its profitability and financial well-being. They are particularly important to:

- They are used by investors to determine whether to sell or purchase a share.

- Creditors, who determine the business ability to pay back debts.

- The management who monitor performance and plans to grow.

- Regulators, who keep companies open and accountable.

Although they are complex in nature, financial statements should be simple and understandable by all stakeholders, including the top management and ordinary consumers.

There are Four Major Classes of Financial Statements

Financial statements are of four main varieties, each with a specific purpose:

- Balance Sheet (Statement of Financial Position)

- Profit and Loss Statement (Income Statement)

- Cash Flow Statement

- Shareholders Equity Statement

In conjunction, they provide a complete account of the financial status of a company, at any one instance and over a specific duration.

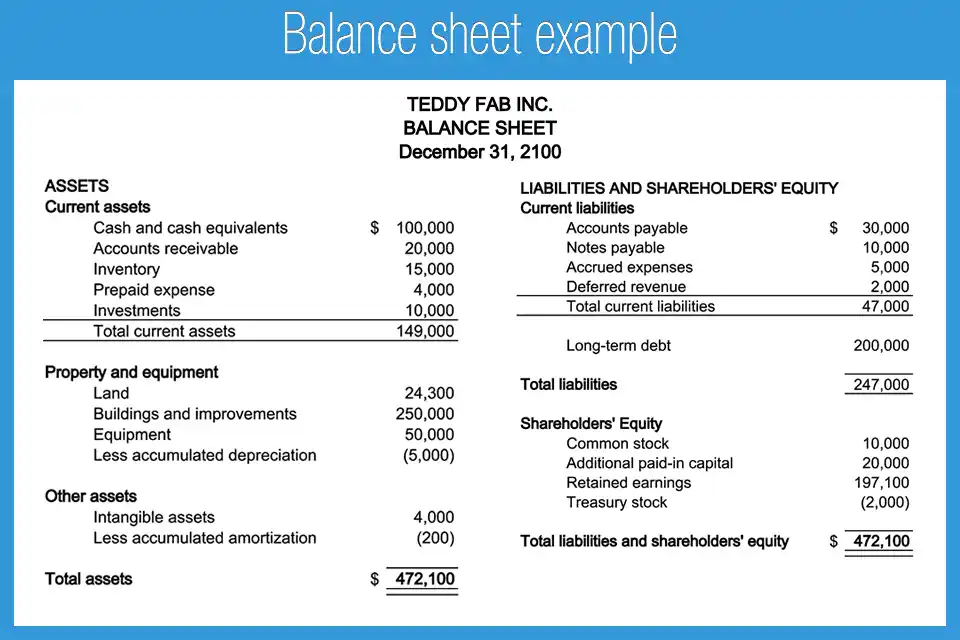

The Balance Sheet: A Financial Position Snapshot

The balance sheet is a summary of what the firm owns (assets), what it owes (liabilities) and what remains to shareholders at a particular moment in time, typically at the end of a quarter or a fiscal year.

The Formula of Balance Sheet

Assets = Liabilities + Equity of shareholders

Assets

The assets are divided into current and non-current (long-term) assets.

Current Assets (which can be converted into cash within one year)

- Cash and Cash Equivalents: Cash, checking accounts, or readily convertible funds

- Accounts Receivable: Customer owed money.

- Inventory: Sales goods or raw materials.

- Prepaid Expenses: Payment of services not yet taken, e.g. insurance or rent.

Non-Current Assets (more than one year)

- Property, Plant & Equipment (PP&E): Buildings, machinery, equipment.

- Intangible Assets: Patents, trademarks, goodwill.

- Long-Term Investments: Securities that are owned over a period of more than one year.

- Deferred Tax Assets: Prepaid taxes that will be reimbursed in the future.

Liabilities

Liabilities are debts that the company owes to others.

Current Liabilities (expiring in less than 1 year):

- Accounts Payable: Money that is owed to suppliers.

- Short-Term Loans: Liability that is payable in less than 12 months.

- Accrued Expenses: Unpaid salaries, taxes, or bills.

- Unearned Revenue: Receipt of money in respect of goods/services not delivered.

Non Current Liabilities (payable after one year):

- Long-Term Debt: Obligations that are bonds or loans to be paid after 12 months.

- Deferred Tax Liabilities: Future taxes.

- Pension Liabilities: Retirement liabilities.

- Lease Liabilities: Long term rental commitments.

Shareholders’ Equity

Equity is the balance of assets and liabilities. It is a form of ownership in the firm.

- Common/Preferred Shares: The amount of shares issued to investors.

- Retained Earnings: The profits that are not paid as dividends but rather retained in the business.

- Treasury Stock: The stock bought back by the company.

- Contributed Surplus & OCI: More paid-in capital and other adjustments that are not reflected in the income statement.

Income Statement: Time-Based Profitability

The profit and loss (P&L) statement is also referred to as the income statement and indicates the revenues, expenses, and profits of a company in a given time (quarter or year). The key items in the income statement are:

- Revenue: The sum of money received as sales or services.

- Cost of Goods Sold (COGS): Direct expenses of producing goods or providing services.

- Gross Profit = Revenue COGS

- Operating Expenses: Rent, utilities, marketing costs, and salaries.

- Operating Income: Gross Profit Operating Expenses

- Net Income: The last profit after all the expenses, taxes and other income/losses.

Comprehensive Income

There are gains and losses that are not shown in the normal income statement, and they include:

- Adjustments of foreign exchange

- Unrealized gains/losses in investments

- Alterations in pension plans

They are reported in Other Comprehensive Income (OCI) and are either reported in a separate statement or as a note.

Cash Flow Statement: Money In and Out

Although the income statement is concerned with profits, the cash flow statement will inform you whether or not the company is generating or losing cash. This sentence divides cash activities into three groups:

Cash Flow Activities

- Operating Activities: The cash received and paid in the course of doing the basic business, including payments made to suppliers and money received by customers. There are non cash items such as depreciation that are excluded.

- Investing Activities: Money used or realized on the acquisition/disposal of assets such as equipment or securities.

- Financing Activities: Cash inflows due to share or loan issue and cash outflow in the form of dividend or repayment of debt.

Direct vs Indirect Method

- Direct Method: Cash inflows and cash outflows are listed directly.

- Indirect Method: Begins with net income and makes non-cash adjustments.

The cash flow statement assists in answering:

- Will the company be able to pay bills?Is it spending cash intelligently to expand?

- Does it require external funding?

Shareholders Equity Statement: Ownership Value Tracking:

This statement describes the variation of equity during the reporting period. It includes:

- Share issue or buy-back

- Profits reinvested (retained earnings)

- Dividends paid

- Other comprehensive income

It demonstrates the amount of value that will be available to shareholders in event of all assets being sold and all liabilities paid.

A positive equity value is an indication of a healthy company whereas a negative value can be an indication of financial distress.

Example: simplified Balance Sheet

To give you an idea, here goes:

Assets

- Cash: 20,000

- Accounts Receivable: 3,000

- Stock: 60,000

- Prepaid Expenses: 11,000

- PP&E: 110,000

- Intangible Assets: 10,000

- Total Assets = 214,000

Liabilities

- Accounts Payable: 2,000

- Accrued Expenses: 1,000

- Long-Term Bank Loan: 100,000

Total Liabilities = 103000

Shareholders’ Equity

- Common Shares: 89,000

- Retained Earnings: 22,000

Total Equity = 111,000

Total Liabilities + Equity = 214,000

Financial Ratios to Analyze

Financial ratios can also be used to analyze performance, which is an aspect of understanding financial statements.

Profitability Ratios

- Net Profit Margin = Net Income / Revenue

- ROA (Return on Assets) = Net Income / Total Assets

- ROE (Return on Equity) = Net Income / Equity

Liquidity Ratios

Current Ratio = Current Assets / Current Liabilities

Efficiency Ratios

Inventory Turnover = COGS / Aver Inventory

Leverage Ratios

Debt-to-Equity = Total Liabilities / Shareholders Equity

Investor Ratios

Earnings Per Share (EPS) = Net Income / Outstanding Shares

Price to Earnings (P/E) = (Stock Price) / EPS

Restrictions of Financial Statements

In spite of its usefulness, financial statements are not without limitations:

- Historical Nature: They present historical information and not forecasts.

- Non-Financial Factors: These include such things as brand reputation or employee morale.

- Inflation Impact: The historical cost accounting may not show the current values of finances.

- Assumptions and Estimates: Comparability may be impacted by various accounting policies.

History of Financial Reporting and Regulations

Following the 1929 crash in stock market, the Securities and Exchange Commission of the U.S. (SEC) introduced audits and standard reporting as a requirement. This was to curb manipulated data and safeguard investors.

Today, Generally Accepted Accounting Principles (GAAP) are used by the U.S. companies, whereas International Financial Reporting Standards (IFRS) are applied by numerous international firms. The standards guarantee uniformity, transparency, and comparability.

What is in an Annual Report?

In an annual report, there is:

- Management Discussion and Analysis (MD&A)

- Financial Statements

- Financial Notes

- CEO/Chairman Letters

- Auditor Reports

- Board Members List

- Risk Analysis and Corporate Strategy

The Art of Reading Financial Statements

This is a simplified method:

- Begin with Income Statement to get profitability.

- Ensure financial stability by looking at the Balance Sheet.

- Look at the Cash Flow Statement to get the true liquidity.

- Analyse the Shareholder Equity to evaluate distribution of value.

- To get more insight and context, scan the Notes and MD&A.

Are All Financial Statements the Same?

Although the basic structure is the same, there are varying accounting standards in different countries:

- GAAP (U.S.)

- IFRS (100+ countries)

- These standards affect the reporting of items such as revenues, inventory and depreciation.

Concluding Remarks: The Importance of Financial Literacy

Financial statements are more than numbers they are the story of a business. As an investor, you want to know where to invest your money; as a creditor, you want to know whether you are at risk of default; as a business owner, you want to know how you are performing. The financial statements are a way to make decisions that are strategic and informed. The skill of reading them does not belong to accountants only. It is an essential tool to anyone who wants to know about the financial world. You can hire The Finance Focus financial consulting experts to that for your business.